The GCC Question: Who Benefits When Knowledge Work Goes Global... and AI Arrives Too?

The map is being redrawn. The question is who gets to draw it.

I have spent a meaningful portion of my career inside the machinery of global capability centers. Building them, staffing them, defending their strategic rationale to skeptical executives, and then watching that rationale evolve in ways no one fully anticipated when the first offshore delivery centers were stood up in the 1990s. The model started as a cost play. It became something more complicated. It is now, in the age of AI, becoming something else entirely.

The GCC question (what these centers are actually for, who benefits from them, and whether the model holds) is one of the most consequential and underexplored threads in the AI-and-work conversation. Most of the coverage is either breathlessly optimistic (GCCs are becoming innovation engines!) or quietly alarmed (AI will hollow them out!). The reality, as usual, is more geographically specific and more structurally interesting than either narrative suggests.

What GCCs Were Built to Do

The original logic was straightforward: skilled labor was cheaper in certain markets, English proficiency was high, infrastructure was improving, and multinationals could build captive delivery operations that gave them more control than third-party outsourcing. India became the epicenter of that model. By the mid-2000s, every major bank, consulting firm, and technology company had some version of an India operation running finance, IT, legal support, HR, or analytics at a fraction of the cost of doing the same work in New York or London.

The model evolved, gradually and then quickly. Cost was still a factor, but the better GCC operations were developing genuine capability — local leaders, institutional knowledge, product ownership, and strategic influence that headquarters increasingly depended on. The narrative shifted from “offshore back office” to “global hub.” And then, just as that repositioning was gaining traction, generative AI arrived and complicated everything.

The Arbitrage Math Is Breaking

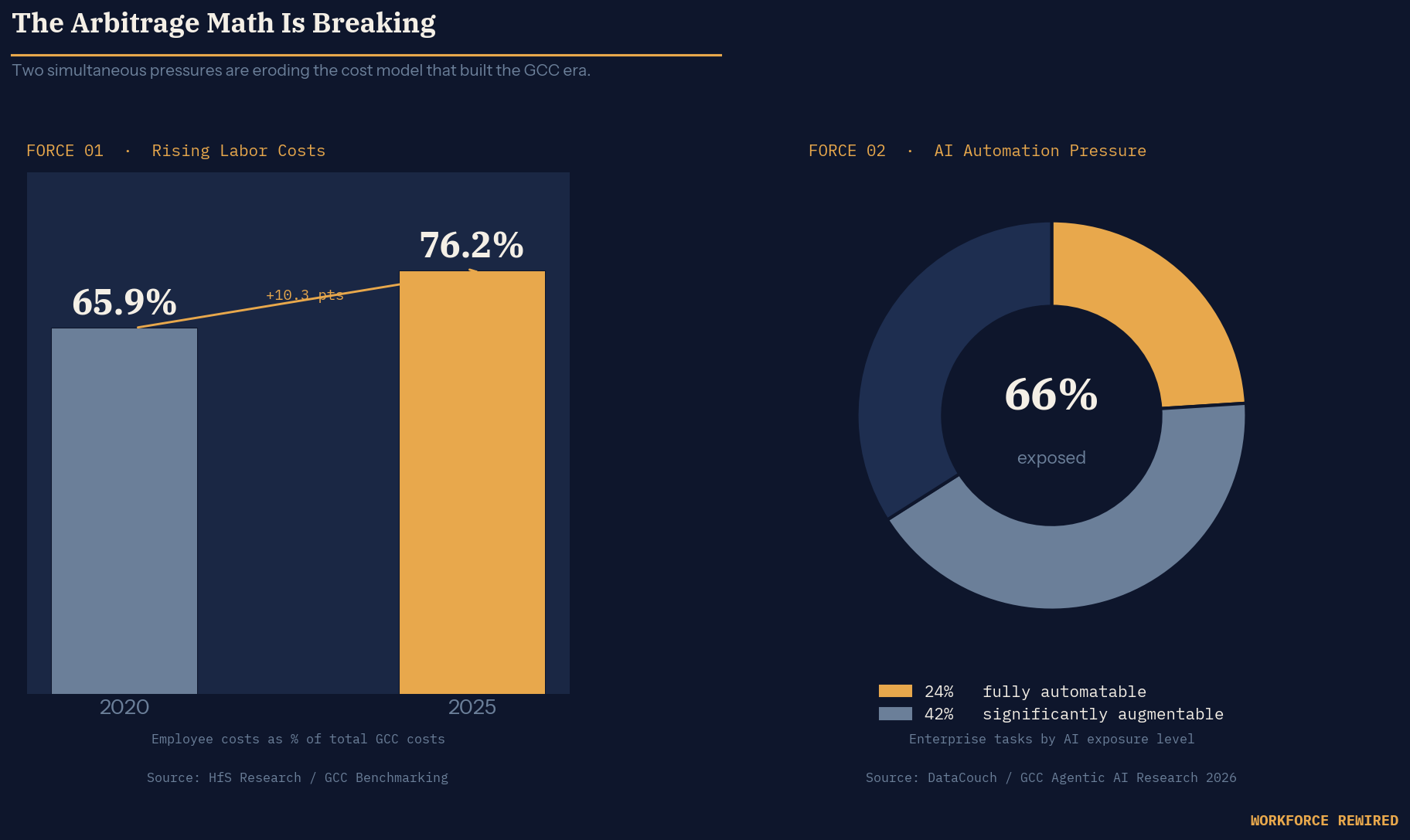

Here is the structural pressure that does not get discussed enough: the cost advantage that anchored the GCC model is eroding from two directions simultaneously.

The first is simple: wages in established GCC markets have risen substantially. Employee costs in Indian GCCs now represent 76.2% of total costs, up from 65.9% in 2020, with salaries projected to increase nearly 10% in 2025 alone. The labor arbitrage that made the model so compelling is compressing. This was already happening before AI. AI is accelerating it.

The second pressure is more structural. AI is automating the category of work that most GCCs were built to perform: routine cognitive tasks — data processing, first-draft document generation, structured analysis, tier-1 support. Research shows 24% of enterprise tasks are fully automatable today, with another 42% significantly augmentable by AI agents. When the work you built your center around is the work that AI does most efficiently, the original headcount rationale starts to unravel.

The GCC leaders who are being honest about this will tell you: the conversation inside their organizations has shifted from “how many FTEs do we have here?” to “what can we build here that AI cannot replace?” That is a genuinely harder question, and the answers are uneven across the map.

India: Still the Center of Gravity, But Reshaping

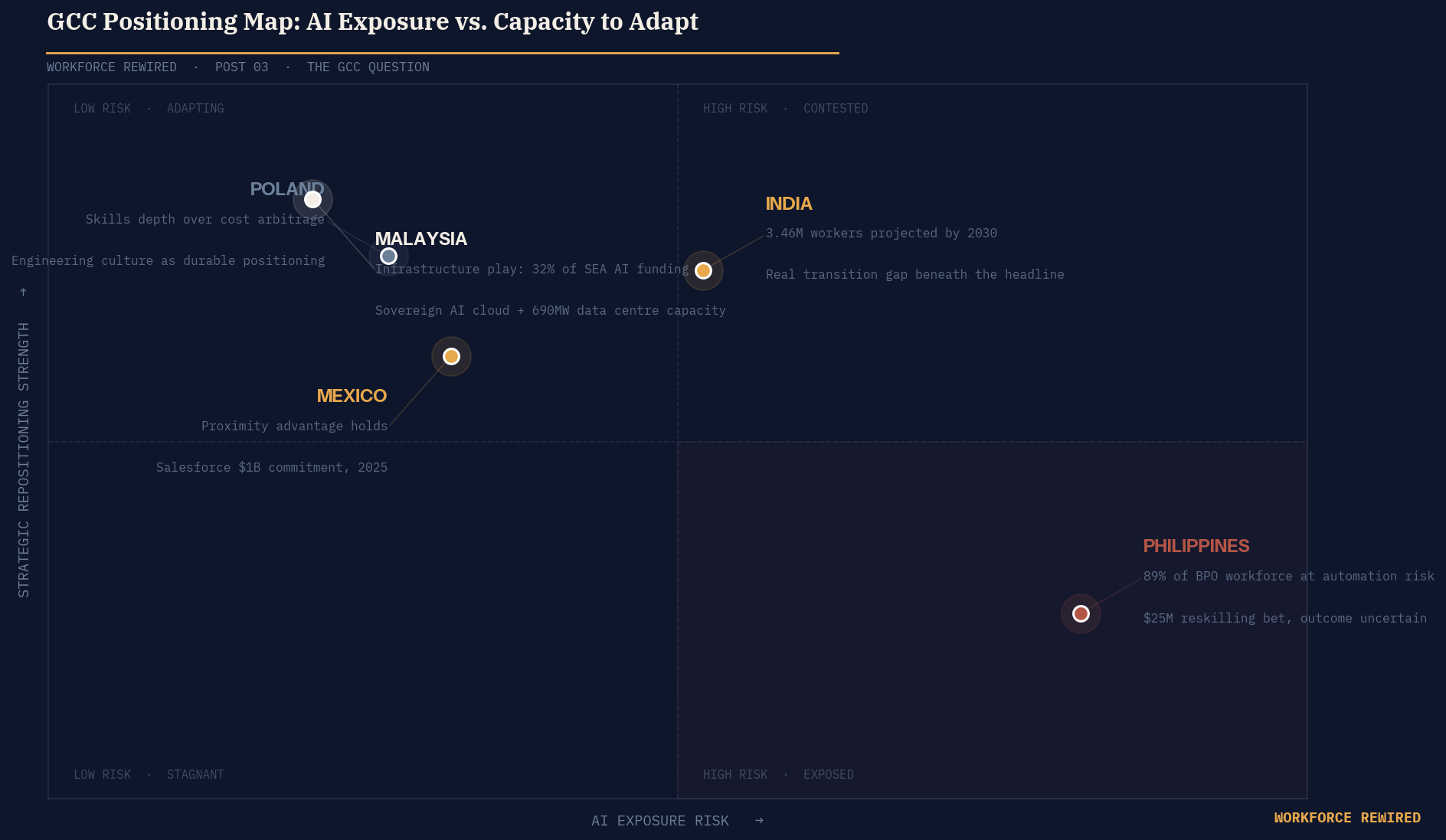

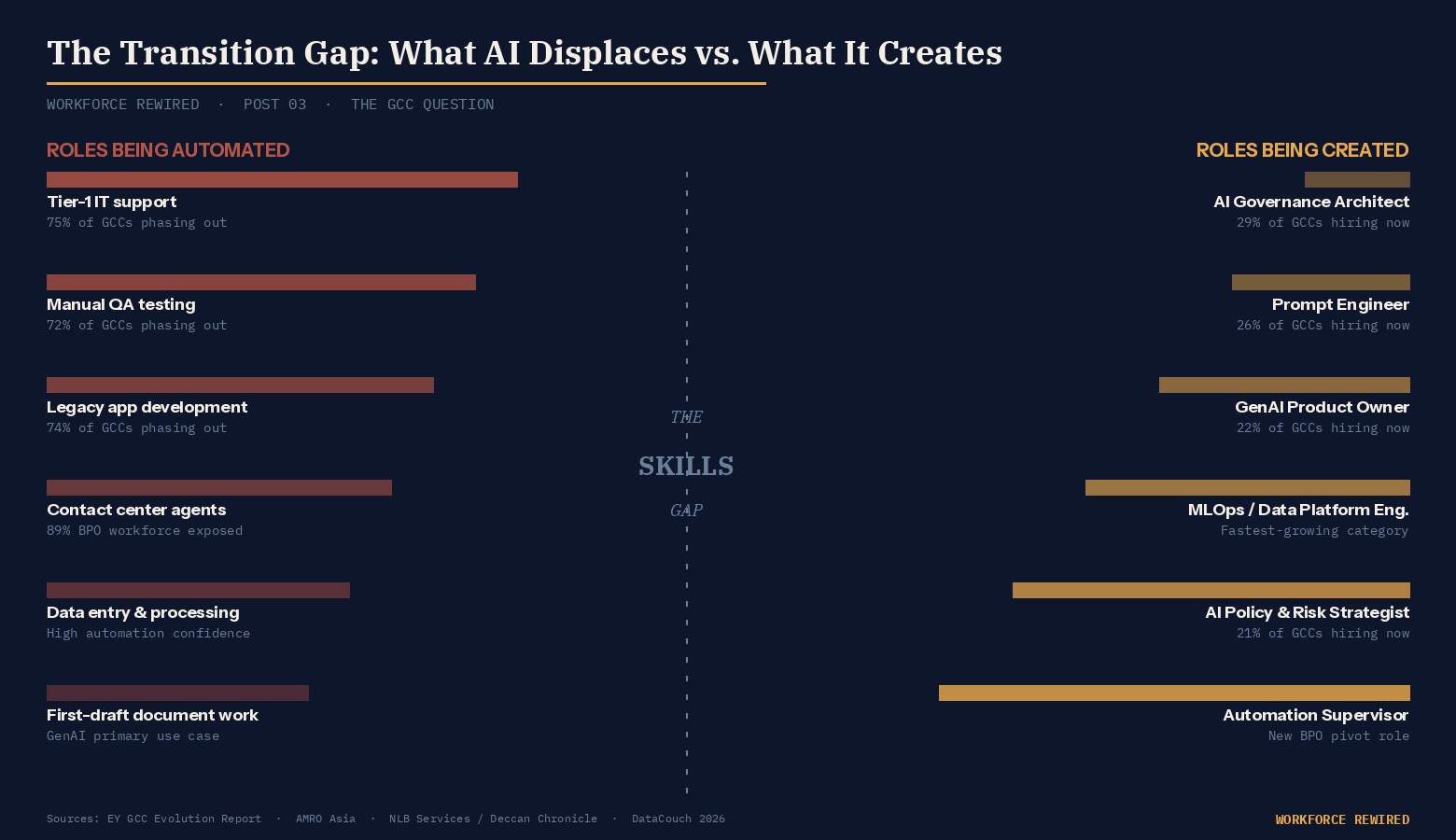

India’s GCC story remains the dominant one, and it will for the foreseeable future. The numbers are staggering: India’s GCC workforce is projected to reach 3.46 million by 2030, adding 1.3 million net new jobs even as legacy roles in L1 IT support, manual QA, and application maintenance are phased out. The EY analysis frames this as India’s GCCs leading a shift to “intelligent, AI-native enterprises” — a repositioning from execution to ownership.

What is making that repositioning possible, at least in part, is a convergence of government ambition and private capital at a scale no other GCC market can match. The Indian government approved the IndiaAI Mission with a total budget of Rs 10,371 crore (approximately $1.2 billion), allocating Rs 2,000 crore in the 2025-26 Union Budget alone, a 1,056% increase over the prior year’s revised estimates. The mission is building out GPU compute infrastructure, funding 80 AI research labs nationwide, and prioritizing domestic AI capability development. Then, in December 2025, Microsoft announced a $17.5 billion investment in India through 2029, its largest commitment in Asia, covering new data center regions, AI infrastructure, and a pledge to train 20 million Indians in AI skills by 2030. Satya Nadella met directly with Prime Minister Modi, and Microsoft signed an MOU with India AI, a division of Digital India Corporation, to advance AI adoption across key sectors.

Hot on Microsoft’s tail followed Amazon with an additional $35 billion investment. Google similarly pledged $15 billion to fund data center expansion, with plans to grow an AI hub in southern India. The combination of sovereign investment and hyperscaler commitment is creating an infrastructure foundation that is genuinely differentiated from anything India’s GCC competitors can point to.

The question worth asking is whether that repositioning is happening fast enough, and for whom. The new roles being created: AI governance architects, prompt engineers, GenAI product owners, machine learning engineers, require a fundamentally different talent profile than the roles being automated away. The tier-1 and tier-2 city graduates who built careers in structured IT support are not automatically the same people who become AI infrastructure architects. The net job number is optimistic. The transition path is not. My experience would tell me to bet on the innovation and rich talent pool in India though.

Malaysia: The Infrastructure Bet

Malaysia represents a different kind of GCC story, one that is less about labor supply and more about physical infrastructure and sovereign positioning.

Malaysia has captured 32% of Southeast Asia’s total AI funding between late 2024 and mid-2025, drawing $6 billion in combined investment from Microsoft, Amazon, and Google. Data center capacity exploded from 120 megawatts in 2024 to 690 megawatts by mid-2025. Johor is becoming Southeast Asia’s fastest-growing data center hub. Prime Minister Anwar Ibrahim has committed RM 2 billion to a sovereign AI cloud and established a National AI Office to coordinate the country’s positioning.

What Malaysia is building is not a traditional GCC workforce story. It is an infrastructure play, positioning the country as the rails on which AI-era knowledge work runs, rather than simply as the location where that work is performed. The jobs that come with data centers are not the same jobs that came with contact centers. There are fewer of them per investment dollar, and they require different skills. But for a country seeking to move up the value chain, controlling the infrastructure layer is a more defensible position than competing on labor cost alone.

I have spent time working in the region, and what strikes me about the Malaysian bet is its clarity of strategic intent. The government is not trying to replicate what India built. It is trying to be the backbone that the next phase of regional work depends on.

The Philippines: A Genuine Reckoning

The Philippines built one of the world’s most successful GCC ecosystems on a specific formula: English fluency, cultural affinity with North American consumers, and a large, educated workforce willing to work night shifts to service U.S. time zones. The country’s BPO and IT-BPM sector accounts for 7.4% of GDP, making it macro-critical in a way few industries anywhere achieve.

The AI exposure is also concentrated: contact center work, which makes up 83% of industry revenue and 89% of employment, is precisely the category of work that AI handles with increasing competence. The IMF has estimated 89% of the BPO workforce faces high automation risk. The industry association, IBPAP, has committed $25 million to reskilling programs and is targeting expansion to nearly two million workers by 2026.

The tension in the Philippines is not hypothetical. It is happening in real time. New AI-adjacent roles like data annotators, automation supervisors, AI trainers are being created, but they are not one-for-one replacements for the contact center agents they accompany. The skills gap is real, the timeline is compressed, and the workers most exposed tend to be young, urban, college-educated women who built middle-class stability on the contact center economy. The equity implications of getting this transition wrong are significant.

Poland: The Differentiated Position

Poland’s story is worth telling because it illustrates what happens when a GCC market builds toward skills depth rather than cost competition.

Poland has roughly 650,000 technology professionals concentrated in Warsaw, Kraków, Wrocław, and the Tri-City area. Salaries are rising with senior developers now earning an average of $73,000 annually, still below Western European peers but no longer dramatically cheaper. The cost gap with London or Amsterdam is narrower than it once was. What Poland has built instead of a pure cost advantage is an engineering culture: deep technical capability, strong university output, and proximity to European headquarters that makes collaboration genuinely easier.

That positioning is proving more durable in the AI era. The GCC operations that will be most affected by automation are the ones running high-volume, low-complexity work. Poland’s GCC ecosystem was never primarily that. The risk for Poland is different: as AI makes senior engineering capacity more abundant globally, does the premium for Polish engineering talent compress? That is a real question. But it is a different problem than the Philippines faces, and the starting position is considerably stronger.

Mexico: Proximity as Durable Advantage

Mexico’s GCC story turns on a fact that AI has not changed and arguably never will: time zones matter.

The nearshore model, building capability centers in Mexico to serve North American companies with real-time collaboration, has a structural advantage that labor arbitrage alone cannot replicate. When the San Francisco engineering team needs to work synchronously with their Guadalajara or Monterrey counterparts, the three-hour maximum time difference is worth something that cannot be automated away. Salesforce committed $1 billion to expanding AI operations and delivery capacity in Mexico City in 2025, reflecting this logic at scale.

What is shifting in Mexico is the talent profile being recruited. The demand is for senior engineers who understand AI and can build with it, not junior developers doing execution work. Mexico has roughly one million developers, but estimates suggest that only 20-25% have the technical depth and bilingual fluency to work effectively in GCC environments (and my experience would tell me that the number is smaller than that). The constraint is not willingness or cost. It is the depth of the talent pool at the specific level these companies want to hire. That is a workforce development problem, and it is one the country is actively working to solve.

What This Map Actually Tells Us

Across these markets, a pattern emerges that complicates both the optimistic and the pessimistic narratives.

The GCC model is not dying. It is differentiating. The markets that built their positioning on labor cost for routine cognitive work are under genuine pressure, and the speed of their repositioning will determine whether AI displacement is managed as a transition or experienced as a collapse. The markets that built on skills depth, infrastructure control, or proximity advantages are in a more defensible position, though not an invulnerable one.

What is consistent across every market is the widening gap between the new roles AI creates and the roles it displaces. The jobs being automated away are accessible, entry-level, and scalable. The jobs being created require credentials, technical fluency, and often years of development investment to fill. That gap is not a market inefficiency that will resolve itself. It is an institutional problem that requires deliberate response from governments, education systems, and employers.

The EY analysis of India’s GCC evolution frames this well: the shift is from labor arbitrage to capability arbitrage (a much more challenging but potentially higher-payoff model). The question is which countries and which workers get to participate in that shift.

The Question No One Is Asking Loudly Enough

Here is what I keep returning to when I think about this landscape...

The GCC model, in its original form, created genuine economic mobility for large numbers of people in developing markets. A young engineer in Bangalore or a contact center agent in Manila or a finance analyst in Kraków built a middle-class life through the transfer of knowledge work across borders. That transfer was imperfect and had costs, but it was also genuinely redistributive. It moved high-value work to places where it created real upward mobility.

AI is now concentrating the value of that work differently. The returns are flowing to the owners of AI infrastructure, to the senior talent who can direct it, and to the companies deploying it. The workers who built the GCC economy by doing the execution work are being handed reskilling brochures and told the new economy will be better.

That may be true in the aggregate and over a long enough time horizon. But the workers in a Manila contact center or a Hyderabad consulting office are not experiencing an aggregate. They are experiencing a specific moment, in a specific job market, with specific skills that the market just repriced.

The architecture of knowledge work is being redrawn. Some countries are positioning themselves intelligently. Some companies are managing the transition with genuine care. But the macro-level optimism about GCC transformation does not automatically translate into good outcomes for the people inside those centers whose work is changing faster than their development pathways are.

The gap between the institutional story and the individual experience is what I think deserves more honest attention. The geography of knowledge work is shifting. The question of who actually benefits from that shift is still very much open.

While I’ve touched on issues specific to GCCs around the world, these reskilling / upskilling challenges they face are not unique. In every geography, this evolution will take a multi-pronged approach for public policy, economic investment by major players, and the willingness for individuals to reinvent themselves.

Next issue: The Upskilling Industrial Complex — why the $300 billion workforce development market is mostly not solving the problem it claims to, and what a better model might actually look like.

If this resonated, share it with someone who is thinking about the future of global work. And if you are building or running a GCC and grappling with these questions in real time, I would genuinely like to hear from you: christina@workforcerewired.co